SCHUFA 2026 update: What it means for you as an expat

On March 17, 2026, Germany finally overhauled its credit system. For anyone moving here, this is a huge deal because the old ‘black box’ that used to decide your financial fate is finally being opened up. Let’s find out more about the new Schufa score methodology together.

What SCHUFA is

What happened in October 2023 and why it matters

How the 12-factor scoring model works

Why the new credit scoring algorithm is good for you

Where to learn more about the credit scoring algorithm

What expats should know in 2026

FAQ – SCHUFA credit scoring algorithm

What SCHUFA is

SCHUFA (Schutzgemeinschaft für allgemeine Kreditsicherung) is the main credit reference agency in Germany. They watch how you handle money to create a creditworthiness assessment that tells businesses whether you're a reliable person. If you're trying to get a phone, a bank account, or fighting for an apartment in a crowded city, your SCHUFA expat credit profile is among the first things Germans look at.

For a long time, expats dealt with a credit history gap problem – if the system didn't know you, it assumed the worst, which made getting started a new life in Germany nearly impossible. Things have started to change now.

What happened in October 2023 and why it matters

The 2026 reforms didn't happen by accident; they were forced by the ECJ Case C-634/21 ruling in October 2023. Previously, the credit rating was fully automatic. Later, the court decided that SCHUFA’s automated decision-making was actually illegal under GDPR Article 22. It’s fair – a computer shouldn't be allowed to ruin your chances of getting an apartment or loan without a human involved.

Because of GDPR compliance, you now have a real ‘right to explanation.’ If a landlord or bank says no because of your score, they have to show their work and let a human review the decision.

How the 12-factor scoring model works

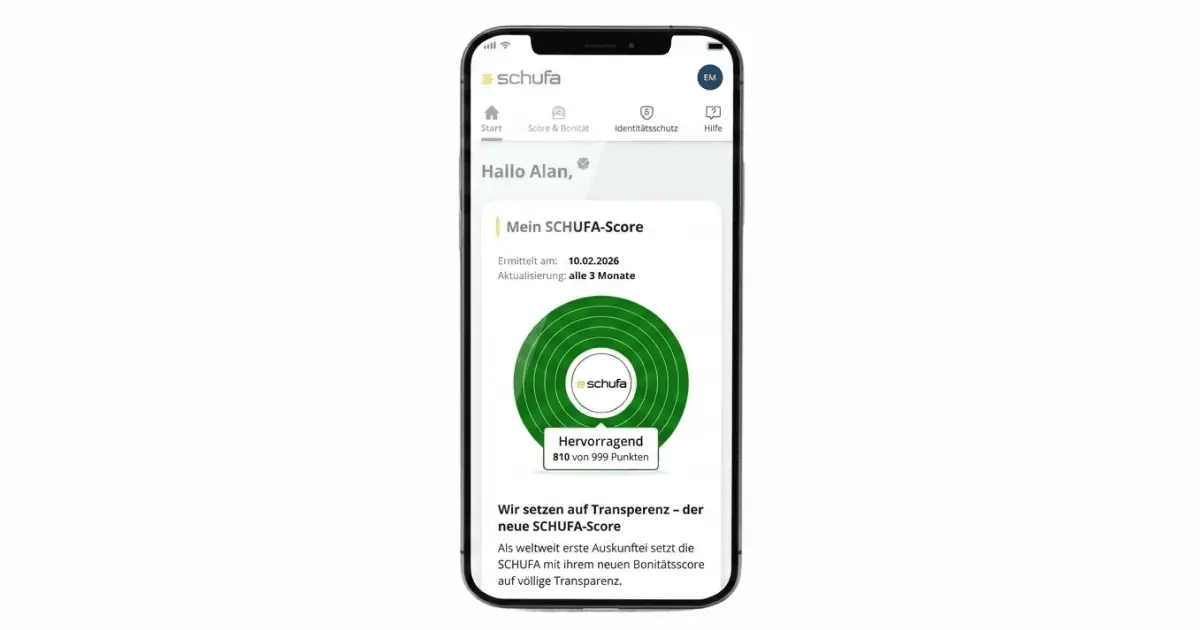

In 2026, SCHUFA ditched its 250 secret variables for a much simpler credit scoring algorithm with just 12 factors. Your Basisscore calculation is now a clear point system from 100 to 999.

12 factors & point values:

| Criterion | Max points | Category |

|---|---|---|

| Payment defaults (No active disruptions) | 264 | Payment history |

| Age of the oldest bank contract | 69 | Account age |

| Age of the oldest credit card | 81 | Account age |

| Age of current address | 94 | Stability |

| Age of most recent line of credit | 36 | Stability |

| Number of bank/card inquiries and transactions | 117 | Activity (12 months) |

| Number of non-bank inquiries (e.g. Telecom) | 99 | Activity (12 months) |

| Instalment loans taken in the last 12 months | 66 | Loans |

| Longest remaining term of all instalment loans | 61 | Loans |

| Credit status (Successfully completed loans) | 19 | Loans |

| Real estate loan / Mortgage | 55 | Loans |

| Existence of an identity check | 38 | Trust |

Here are some example explanations of what’s actually hidden behind these criteria:

- Paying on time (264 pts): As long as you don't have a major unpaid bill (a negative entry), you keep these points.

- Your address (94 pts): Every year you stay in the same apartment, this score goes up. Moving every six months makes the system nervous.

- Your first bank account (69 pts): The longer you keep your first German bank account open, the better.

- New loans (66 pts): When you take out a new loan, your score drops temporarily because you have a new debt to pay.

- The ID check: As soon as you do a formal ‘Identity Check’, you get these points.

You can read more about all the criteria and approximately calculate your score on the official SCHUFA website.

Why the new credit scoring algorithm is good for expats

- Stability over ‘ghosting’. It used to be that having no history made you ‘high risk,’ but now, simply proving who you are and where you live via Anmeldebestätigung (residence registration) gives you 'trust points' immediately.

- Ending the 'neighbourhood penalty'. Before 2026, GDPR automated profiling often used 'geo-scoring' – basically judging you based on where you lived if they didn't have your data. That's over. Now you're judged on your own ID, and how long you've lived at your address, so you aren't punished for your neighbours’ unpaid bills.

- Faster 'Score recovery' for small mistakes. It’s easy to miss a gym bill when you’re moving countries. Under the new BDSG (Bundesdatenschutzgesetz), if you pay off a small mistake within 100 days, it’s cleared from your record in half a year. Much faster than the old 3-year penalty.

- EU expat vs non-EU expat scoring. While registration hurdles used to differ, the unified identity checkpoints (38 pts) ensure that your origin matters less than your verified presence in Germany.

Where to learn more about the credit scoring algorithm

The reform launched a new app and portal so you can see your data whenever you want.

- Selbstauskunft: This is your free legal right under the GDPR to get a copy of your data for free.

- The simulator: Inside the meineSCHUFA.de self-inquiry portal, you can now test-drive financial moves – like moving house or getting a loan – to see exactly how many points your score will drop or gain before you do it.

What expats should know in 2026

- Keep your first account: Since the 'Age of oldest bank contract' is worth 69 points, don't close your first German bank account. Let it sit there as an anchor for your score.

- Verify your ID: Do the Post-Ident process the moment you get your residence permit. It’s an easy 38 points that many people forget to claim.

- Batch your applications: If you need a phone, internet, and a credit card, do it all in the same month. Because of the 28-day rule, multiple inquiries in a short window count as one.

- Ask for a 'Condition Request': When shopping for loans, always ask for a Konditionsanfrage. Unlike a Kreditanfrage, this lets you compare prices without hurting your score.

- Watch the '0% financing': Buying a sofa and a phone on separate tiny payment plans looks messy. It’s actually better for your score to have one larger loan than five small ones.

- Check your spelling: Make sure your name on your Anmeldebestätigung matches your bank and bills perfectly. If it doesn't, SCHUFA might create two broken profiles for you, and neither will have a good score.

These tips are all valid as of March 2026. Keep an eye on SCHUFA updates because some rules may change over time.

Moving to Germany or already living there? Check these articles for expats:

FAQ – SCHUFA credit scoring algorithm

Are EU and non-EU expats treated differently under the new SCHUFA rules?

Everyone gets the same protections against automated decision-making now, but EU citizens often have an easier time because their data moves more freely across borders. For non-EU expats, your expat financial inclusion depends more on your German activity, like your registration and local bank history, since foreign data is harder for SCHUFA to verify.

How can I check my SCHUFA score for free, and what should I look for?

You can get a free 'Data Copy' (Selbstauskunft) once a year at meineSCHUFA.de to see exactly what’s on your record. Check for simple errors like wrong addresses or old, closed accounts that are still listed, as these mistakes can quietly hurt your credit history and, therefore, rental market access.

How can I build or protect my SCHUFA score?

Stay consistent: a long-term address and a single, old bank account are worth a lot of points. Use the new 'Simulator' tool to see how a new credit card or loan might change your score before you actually apply for it.

Will the SCHUFA update guarantee me access to credit or housing?

Not exactly – it just guarantees that you won't be rejected by a computer without a human looking at your case. While it stops unfair 'black box' rejections, landlords and banks still have the final say based on your income and overall reliability.

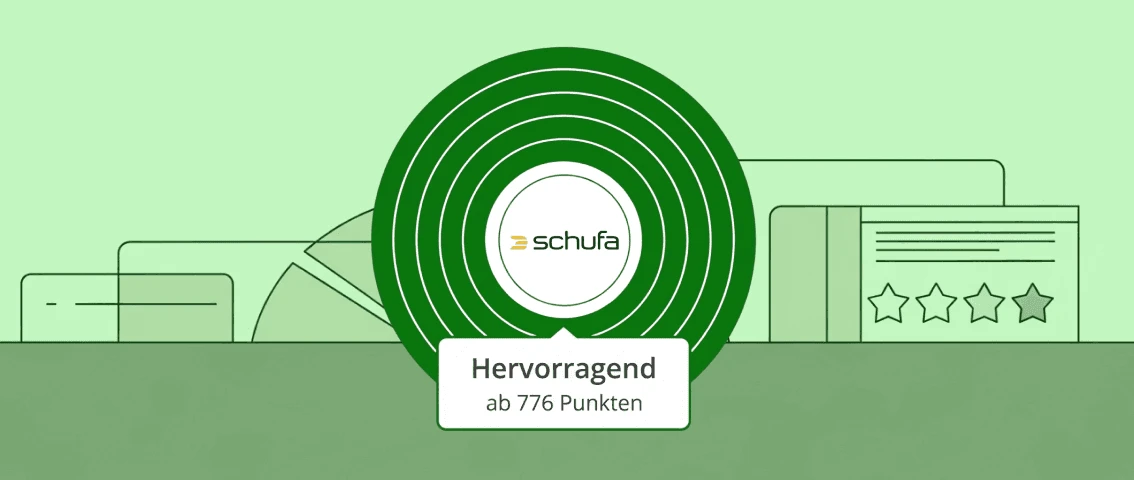

Which SCHUFA score is good?

There are five SCHUFA score classes.

- Unsatisfactory: Below 100 points (no score)

- Sufficient: 100 to 641 points

- Acceptable: 642 to 708 points

- Good: 709 to 775 points

- Outstanding: 776 to 999 points

Most people in Germany fall in the ‘Outstanding’ class, so you need to aim high.